5 steps towards a financially fit retirement

If retirement is just around the corner, the current financial climate may make you feel a little uneasy. Watching the markets fluctuate might leave you worrying about whether your superannuation will be enough to see you through.

It’s not a time for hasty moves, though.

If you are concerned a calm review of your current portfolio and investment strategy may be helpful.

After all, the average Australian spends around 20 years in retirement, so it’s important to create a retirement strategy that takes account not only the current market conditions but also the risks and opportunities in the years ahead.

As one of the most significant retirement assets, your superannuation needs a carefully considered assessment as you approach any new life stage.

Here are five useful tips to help ease you into the next chapter towards retirement.

1. Review your risk profile and portfolio allocation

Check your super portfolio’s risk profile. Generally speaking, investors take a high-growth approach when they’re younger to take advantage of higher returns, however, as with normal share market cycles, there will be fluctuations in the share market. Having a long-term strategy gives you the time to recover from any market downturns before retirement.

Older investors may prefer a more conservative investment strategy that can help to stabilise returns by potentially protecting super from share market volatility.

2. Calculate retirement expenses

Be realistic about the living expenses you’ll need when you finish working. For some, it may cost less to live in retirement because of reduced expenses such as commuting costs and maintaining a work wardrobe.

On the other hand, you may plan to travel more or buy a new vehicle or renovate your home, so these expenses need to be factored in when working out how much you’ll need.

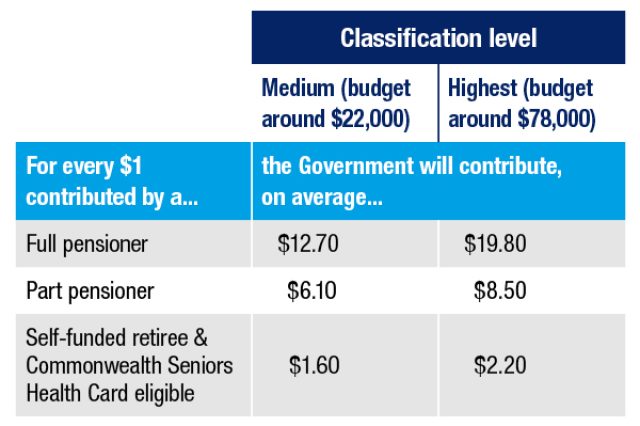

According to the Association of Superannuation Funds of Australia (ASFA), the annual average budget to maintain a comfortable lifestyle in retirement is $73,077 for a couple and $51,805 for a single person.i

And to maintain a modest lifestyle, ASFA estimates a couple will need $47,470 and a single person will need $32,897. Both estimates assume you already own your own home.

You can find easy-to-use tools on the MoneySmart website to help you work out your budget and also estimate your income from super and the Age Pension.

3. Take action on mortgages and loans

Entering retirement with manageable or small levels of debt can contribute to feeling more financial stable.

If you’ll still be repaying a mortgage after you’ve retired, you could consider downsizing your home or using superannuation funds to pay down the debt, keeping in mind the tax implications and ensuring that you comply with superannuation laws. If you’re considering either of these courses of action, we’d be happy to explain your options and obligations.

4. Check your timing

Understanding when and how you can access your super is important.

You can use your super to fund your retirement when you reach “preservation age”, which is from age 60. You can also use your super to begin a transition to retirement income stream (TRIS) while continuing to work.ii

Alternatively, if you continue working beyond preservation age, you can withdraw your super once you turn 65.

There are also some circumstances in which you can access your super early such as illness and financial hardship, however, eligibility requirements do apply.iii

5. Decide how to withdraw your funds

You may be able to withdraw your super in a lump sum, if your fund allows it. This could be the entire amount you have invested, or you could receive regular payments.

If you ask your fund for regular payments (paid at least once a year), it is known as an income stream and your super account transitions from the accumulation phase – where contributions are made – to a pension.

There are minimum withdrawals that you must make once you commence an income stream from super. For example, for those aged under age 65, a minimum annual withdrawal of 4 per cent of your super balance is required and this drawdown rate increases as you get older.iv

There is a lot to think about as you approach retirement, so if you’d like to discuss your retirement income options, please give us a call.

i ASFA Retirement Standard, December 2024 – The ASFA Retirement Standard – ASFA

ii Super withdrawal options | Australian Taxation Office

iii When you can access your super early | Australian Taxation Office

iv Payments from super, April 2025 – Payments from super | Australian Taxation Office